AI Selloff and Payroll Surprise Push Treasury Yields Back to One-Year Highs as BlackRock Calls for New Portfolio Approach

- Jun 9

- 7 min read

Weekly Market Commentary | Week of Jun 8th, 2026

A Recap of Economic and Financial Trends from the Prior Week

By: Michael Horvath, The Quinnipiac University Global Economics Research Team

Last Week in Review

U.S. nonfarm payrolls beat estimates by a wide margin and ISM Manufacturing hit a four-year high, though jobless claims rose to their highest level since February and the eurozone's Q1 GDP was revised to a contraction

A sharp selloff in chip stocks drove the Nasdaq's steepest weekly decline since March as Treasury yields climbed back to one-year highs following the payrolls report, with the Dow Jones Industrial Average the only major index to hold near flat

BlackRock argues the AI mega force has structurally reshaped indexes and bond markets, requiring a new portfolio approach built around exposures rather than asset class labels

Economic Recap

U.S. economic data last week pointed to continued labor market resilience alongside persistent inflationary pressures. The Bureau of Labor Statistics reported that the U.S. economy added 172,000 jobs in May, well ahead of consensus estimates for around 80,000, while April's reading was revised upward to 179,000 from 115,000, with job growth led by gains in leisure and hospitality, local government, and health care. The unemployment rate was unchanged at 4.3%. The Labor Department also reported that job openings rose to 7.618 million in April, well above expectations for around 6.79 million and the highest level in nearly two years, while ADP reported that private employers added 122,000 jobs in May. However, initial jobless claims for the week ended May 30 rose 13,000 to 225,000, the highest reading since early February, and Challenger, Gray and Christmas reported that announced layoffs at U.S. employers rose 16% from April to approximately 97,000, with companies citing AI as the leading reason for job cuts for the third consecutive month. The ISM Manufacturing PMI rose 1.3 points to 54.0 in May, its highest level in four years, with new orders expanding for the fifth consecutive month, while the ISM Services PMI also beat expectations, rising to 54.5 from 53.6, with the prices index climbing to its highest level since August 2022. The Federal Reserve's Beige Book noted increased activity in 10 of 12 Fed districts while highlighting that prices increased at a moderate to strong pace overall.

Internationally, final data from Eurostat showed the eurozone economy contracted 0.2% in Q1 2026, a downward revision from an initial estimate of 0.1% growth, with the sharpest decline in Ireland where the economy contracted 12.1%. Eurozone retail sales fell 0.4% sequentially in April, below the already-weak consensus estimate for a 0.3% drop. ECB board officials publicly signaled that a June interest rate hike is likely. In Japan, nominal average wages rose 3.5% year over year in May, above the 3.2% increase anticipated and marking the fourth consecutive month of positive real wage growth, while household spending contracted 0.5% year over year in April, extending a five-month declining trend. The yen weakened to around JPY 160 against the U.S. dollar, prompting fresh verbal warnings from Finance Minister Satsuki Katayama, while the Ministry of Finance confirmed that foreign exchange interventions totaling JPY 11.735 trillion were conducted between April 28 and May 27. In China, the official manufacturing PMI eased to 50.0 in May from 50.3 in April, while the private RatingDog China General Manufacturing PMI remained in expansion at 51.8.

Market Recap

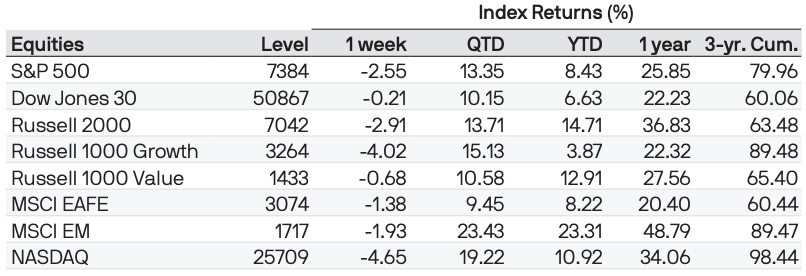

Source: JPMorgan Asset Management, “Weekly Market Recap” (June 8th, 2026). (Chart © JPMorgan Asset Management. Chart used under fair use for educational commentary by The Quinnipiac Global Economics Research Team.)

Major U.S. stock indexes finished the week lower as early gains tied to AI optimism faded amid oil price volatility, a stronger-than-expected payrolls report, and elevated earnings expectations for AI-linked companies that raised concerns about valuations. The Nasdaq Composite led declines, falling 4.65% on the week to 25,709 and giving back a meaningful portion of its recent advance; the index is now up 10.92% year to date. The Russell 2000 fell 2.91%, the S&P 500 declined 2.55% to 7,384 and is up 8.43% year to date, ending roughly 3% off its all-time high following the chip stock selloff. The Russell 1000 Growth dropped 4.02% and is now up only 3.87% year to date while the Dow Jones Industrial Average held up best, slipping just 0.21% on the week and remaining up 6.63% year to date. The Russell 1000 Value declined a more modest 0.68% and remains up 12.91% year to date, continuing to outperform growth substantially on a year-to-date basis. U.S. Treasuries generated losses on the week, with the 10-year yield rising to around 4.55% from 4.44% the prior week as solid economic data and hawkish Fed commentary fueled concerns that monetary policy would remain restrictive for longer. Investment-grade corporate bond issuance ran at its fastest pace year to date since 2020, though new issues were generally oversubscribed. Brent crude settled near USD 94 per barrel.

Internationally, the MSCI EAFE fell 1.38% on the week and is up 8.22% year to date, while MSCI EM declined 1.93% and is up 23.31% year to date. The pan-European STOXX Europe 600 declined 0.53% in local currency terms, with Germany's DAX falling 1.38%, Italy's FTSE MIB slipping 0.29%, and the UK's FTSE 100 losing 0.40%, while France's CAC 40 edged up 0.43%. Japan's Nikkei 225 gained 0.39% while the broader TOPIX fell 0.20%, as elevated energy prices kept inflation risks and interest rate expectations in focus. China's CSI 300 fell 1.54% and the Shanghai Composite declined 1.00%, while the Hang Seng retreated 0.88%.

Market Themes

The AI Mega Force Demands a New Portfolio Construction Framework Built Around Exposures

BlackRock Investment Institute argues that the fast-changing investment landscape driven by mega forces, most prominently artificial intelligence, necessitates a fundamentally new portfolio approach built around underlying economic exposures rather than traditional asset class labels. The core observation is that the share of the information technology sector in the MSCI U.S. index has roughly doubled since the launch of ChatGPT in 2022, rising from approximately 23% to approximately 38%, while the IT sector's share of the MSCI Emerging Markets index has also roughly doubled from approximately 19% to approximately 44%, and its share of U.S. investment grade bond issuance has more than tripled from approximately 6% to approximately 20%. This means that investors relying on traditional geographic or asset class labels are inadvertently accumulating concentrated AI exposures across what appear to be diversified portfolios. BlackRock's framework calls for revisiting big portfolio calls more frequently, maintaining an explicit plan B portfolio, shifting the unit of analysis to underlying economic and factor drivers of return and risk, and taking a more holistic approach to risk budgeting between alpha and beta. The firm notes that equity investors at its Midyear Forum highlighted that geography is no longer a major input for investment decisions, with what a company actually does and the drivers of its revenue mattering more than the country where its stock is listed.

China's AI Commercialization Push and Indonesia's Market Stress Highlight Emerging Market Divergence

Emerging market performance last week was shaped by two divergent developments that underscore the differentiated risk landscape across the asset class. In China, investor attention shifted toward AI commercialization, with Tencent Holdings reported to be testing an embedded AI agent for WeChat, China's largest social media and payments platform, and potentially beginning regulatory approval as early as this month. Separately, AI startup DeepSeek is exploring a fundraising round that could value the company at approximately USD 52 billion, underscoring the growing focus on moving from AI model development toward commercial deployment across Chinese technology. By contrast, Indonesia emerged as one of the weaker markets in Asia, with equities falling to a four-year low and the rupiah weakening to record lows as higher oil prices raised concerns about inflation, subsidy costs, and pressure on external balances. The combination of revisions to Bank Indonesia's mandate that broadened its objectives to include support for economic growth, a sharp equity decline following fresh U.S.-Iran military exchanges on Wednesday, and rupiah weakness to record levels illustrates how geopolitical and policy uncertainty are producing sharply divergent outcomes across the emerging market universe even as aggregate EM indexes retain meaningful year-to-date gains.

Chart of the Week

Source: BlackRock Investment Institute, with data from Bloomberg and Dealogic (ION Analytics), "Looking Through Labels: IT Sector Share of Selected Equity and Bond Indexes, 2022 and 2026," June 2026. (Chart © BlackRock Investment Institute. Used under fair use for educational commentary by The Quinnipiac Global Economics Research Team.)

The chart compares the information technology sector's share of the MSCI U.S. index, the MSCI Emerging Markets index, and U.S. investment grade bond issuance at two points in time: 2022 and 2026. In the MSCI U.S., the IT sector's share rose from approximately 23% in 2022 to approximately 38% in 2026. In the MSCI EM, it rose from approximately 19% to approximately 44%. In U.S. investment grade bond issuance, IT's share rose from approximately 6% to approximately 20%, more than tripling over the period. BlackRock uses this chart to illustrate that taking thematic exposures in portfolios requires a lens that transcends asset class labels, as the AI-driven growth of technology has permeated equity indexes and fixed income markets simultaneously and to a degree that is not captured by traditional geographic or asset class categorizations. The data reinforce the firm's argument that all asset allocation decisions are now active calls and that portfolios must be built around exposures and convictions rather than conventional labels.

Market Outlook

BlackRock Investment Institute will closely watch U.S. May CPI and PPI data this week for evidence of how the ongoing Strait of Hormuz supply shock is affecting already sticky price pressures, noting that the full breadth of the shock has yet to show and will depend on how the conflict evolves. BlackRock warns that a prolonged closure into July could bring the impact of the shock more prominently to the fore, particularly as U.S. oil inventories could potentially hit four-decade lows. New Federal Reserve Chair Kevin Warsh's first policy meeting as chair this week will be closely watched, with markets focused on how he addresses the combination of strong job growth, an uptick in job vacancies, and mounting wage pressure. China's CPI and PPI data are also in focus, with weak domestic demand expected to continue running alongside firming factory gate prices. The Trump administration's announcement of 10% to 12.5% tariffs on many countries adds a further layer of uncertainty to the global trade outlook heading into the second half of the year.

Calendar Events

Economic Data

Jun. 9 (Tue): U.S. trade balance (Apr); China trade balance (May)

Jun. 10 (Wed): U.S. CPI (May); China CPI and PPI (May)

Jun. 11 (Thu): U.S. PPI (May); Federal Reserve policy decision

Jun. 12 (Fri): UK GDP (Apr)

Major Corporate Earnings

Jun. 10 (Wed): Oracle Corporation (Q4 2026)

Jun. 11 (Thu): Adobe Inc. (Q2 2026)

Sources

J.P. Morgan Asset Management. "Weekly Market Recap PDF." J.P. Morgan Asset Management. https://am.jpmorgan.com/content/dam/jpm-am-aem/americas/us/en/insights/market-insights/wmr/weekly_market_recap.pdf

J.P. Morgan Asset Management. "Economic Update." J.P. Morgan Asset Management. https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/market-updates/economic-update/

T. Rowe Price. "Global Markets Weekly Update." T. Rowe Price Insights. https://www.troweprice.com/personal-investing/resources/insights/global-markets-weekly-update.html

BlackRock Investment Institute. "Weekly Investment Commentary: The Need for a New Portfolio Approach." BlackRock, June 8, 2026. https://www.blackrock.com/us/individual/literature/market-commentary/weekly-investment-commentary-en-us-20260608-the-need-for-a-new-portfolio-approach.pdf

BlackRock Investment Institute. "Weekly Commentary Archives." BlackRock. https://www.blackrock.com/corporate/insights/blackrock-investment-institute/archives

Apollo. "The Daily Spark." Apollo. https://www.apollo.com/wealth/the-daily-spark

MarketWatch. "Economic Calendar." MarketWatch. https://www.marketwatch.com/economy-politics/calendar

Yahoo Finance. "Earnings Calendar." Yahoo Finance. https://finance.yahoo.com/calendar/earnings/

Comments