CEE Exchange Rates Report for December 2nd – 6th

- Jan 6, 2025

- 2 min read

By: Zoe McLaughlin, The Quinnipiac University Economics Research Team

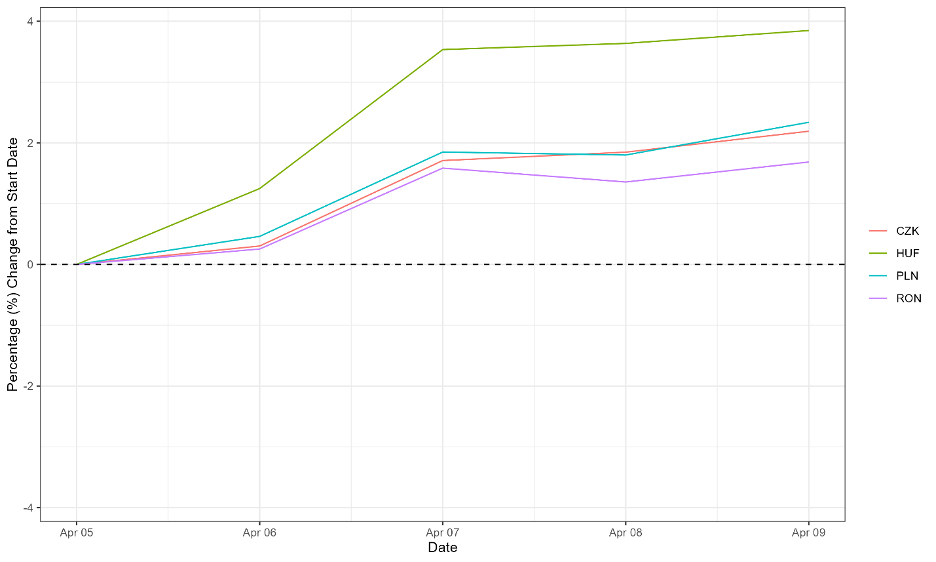

CEE Currencies Index

Source: Eurostat and own calculations. Exchange rates are inverted to be USD per local currency (i.e., an increase indicates a stronger domestic currency) and then indexed to 100 at the start of the period.

During the week of December 2 – December 6, the Czech koruna (red), Polish złoty (blue), and Romanian leu (purple) decreased in value relative to the United States dollar, but the Hungarian forint (green) increased in value relative to the United States dollar. The Romanian leu ended the week with the least change, at a decrease of -0.18%, but reached a mid-week high of 0.66% on December 4. The Czech koruna ended the week at a decrease of -0.76%, with a mid-week high of 0.56% on December 2. The Polish złoty experienced the most significant decrease, ending this week at a decrease of -0.85%, with a mid-week high of 0.51% on December 3. The Hungarian forint ended the week at an increase of 0.45%, with a mid-week high of 1.31% on December 4.

CEE Currencies Historical Trends

Source: DBNomics and own calculations. Exchange rates are inverted to be USD per local currency (i.e., an increase indicates a stronger domestic currency). The center line is a rolling three-month average. The upper and lower boundaries are the average plus and average minus one standard deviation, respectively, for the same three-month period.

The Hungarian forint and Romanian leu are both over one standard deviation below their three-month rolling averages, and the Czech koruna and Polish złoty are less than one standard deviation below their respective three-month averages. All four currencies have demonstrated a significant decline since September. Since the beginning of December, the Czech koruna, Polish złoty, and Romanian leu have been exhibiting slight increases. The Hungarian forint has remained relatively stable for the past few weeks, but still significantly lower than its September value.

Further Reading

Over the first three quarters of this year, the Romanian economy significantly underperformed expectations, with the GDP only growing by 0.9% so far this year. However, government spending has been higher than normal due to tumultuous elections. Decreasing agricultural output due to ongoing drought as well as struggles in the nation’s IT sector have been contributing to the stifling of Romania’s growth. Additionally, inflation is projected to increase through the end of 2024. Romania also is maintaining a significant trade deficit, primarily fueled by food, fuel, and manufactured goods.

At their December meeting, the Monetary Policy Council of Poland’s national bank voted to leave interest rates unchanged, with the current policy rate at 5.75%. The council’s post-meeting statement included updates on the Polish economy, indicating that GDP data was weak during the third quarter, but industrial production and retail sales were improved. Overall, inflation remains high due to price increases in the services sector. Currently, Poland’s energy prices are frozen, which has been taming inflation, but that freeze expires at the end of September 2025, which may accelerate inflation.

Comments