CEE Exchange Rates Report for November 10th – 14th

- Nov 16, 2025

- 3 min read

By: Margaret Gachau, The Quinnipiac University Global Economics Research Team

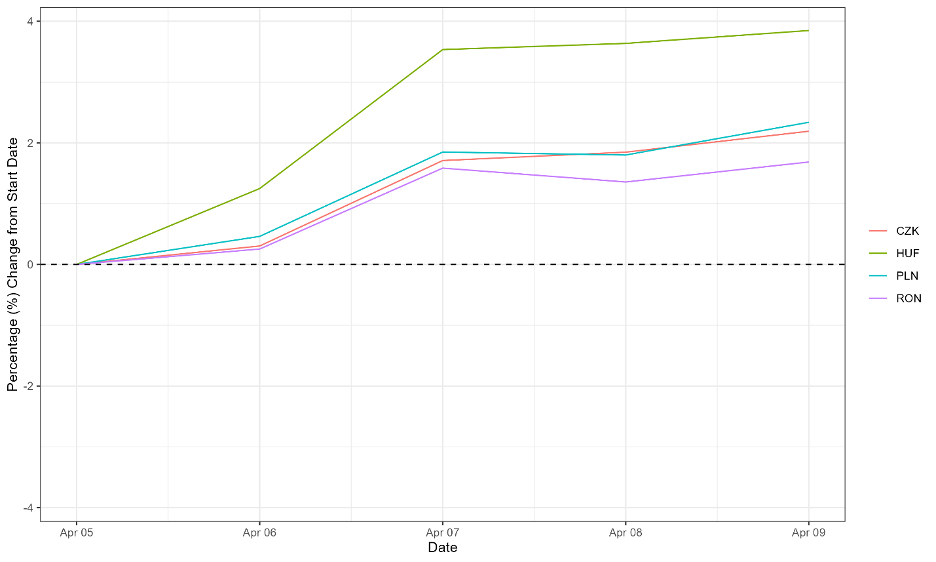

CEE Currencies Index

Source: Eurostat and own calculations. Exchange rates are inverted to be USD per local currency (i.e., an increase indicates a stronger domestic currency) and then indexed to be 100 at the start of the period.

During the week of November 10, 2025 – November 14, 2025, the CEE currencies depreciated notably against the U.S. dollar, extending the losses observed in the previous week. Except for the Hungarian forint (green), they all trended downward till November 11th where they all had renewed weakness set in towards the end of the week. Romanian leu (purple) emerged as the strongest performer, experiencing relatively smaller losses and ending the week at approximately -0.75%, supported by lower volatility compared to others. The Hungarian forint (green) followed a different path, briefly recovering to near -0.05% on November 11th, then declining again to finish at roughly -0.9% ranking the second strongest at the end of the week. The Polish zloty (blue) displayed steady depreciation throughout the period, declining to approximately -1.1% making it the second weakest performer of the week. The Czech koruna (orange) was the weakest performer overall, following a similar downward trajectory of the other currencies ending the week down by approximately -1.3%, showing the most significant depreciation among all four currencies during this period.

CEE Currencies Historical Trends

Source: Eurostat and own calculations. Exchange rates are inverted to be USD per local currency (i.e., an increase indicates a stronger domestic currency. The center line is a rolling three-month average. The upper and lower boundaries are the average plus and average minus one standard deviation, respectively, for the same three-month period.

During the mid-week of November 2025, the CEE currencies showed signs of sustained recovery following the previous weeks’ slight upward adjustments, with each currency displaying varying degrees of strengthening. The Czech koruna (CZK) appreciated toward the upper end of its three-month rolling average moving above 0.05, indicating a mild but notable improvement. The Hungarian forint (HUF) followed a similar path, rising steadily surpassing the upper boundary of its rolling three-month average near 0.003. The Polish zloty (PLN) also strengthened, climbing above its mid-range level moving to 0.28 reflecting a gradual appreciation through mid-November. Meanwhile, the Romanian leu (RON) continued to exhibit limited volatility showing limited upward momentum, recording an exchange rate just above its lower boundary; 0.23, remaining the weakest performer among the four.

Additional Readings

This article outlines the upcoming drivers of global and CEE market sentiment, noting that the U.S. economy is still normalizing after the government shutdown, with delayed jobs data and Federal Reserve minutes likely to dampen expectations for a December rate cut. In Central and Eastern Europe, Hungary’s central bank is expected to keep interest rates unchanged while maintaining a stance to offset pro-inflationary fiscal easing. In the Czech Republic, weak external demand continues to pressure industrial prices, with lower input costs supported by a stronger koruna. The overall outlook suggests that both global and regional monetary policy expectations will play a key role in shaping financial market movements in the days ahead.

This article provides further overview of recent economic developments across Central and Eastern Europe (CEE), highlighting how differing growth trajectories and shifting monetary policies are shaping regional outlooks. Poland is experiencing solid growth alongside faster-than-expected disinflation, prompting the central bank to front-load rate cuts. The Czech economy remains stable but vulnerable to weak external demand, despite resilient consumer spending. Hungary continues to face stagnation, with muted activity and only limited scope for future policy easing, while Romania struggles with subdued growth and persistent inflation pressures. Overall, the report suggests that diverging fundamentals and increasingly dovish signals across the region may influence currency performance, particularly in an environment where global conditions remain uncertain.

Comments