Strait of Hormuz Reopens as Record Highs Return and AI Capital Spending Estimates Surge

- Apr 21

- 6 min read

Weekly Market Commentary | Week of Apr 20th, 2026

A Recap of Economic and Financial Trends from the Prior Week

By: Michael Horvath, The Quinnipiac University Global Economics Research Team

Last Week in Review

Iran declared the Strait of Hormuz open during the Lebanon ceasefire, sending oil sharply lower and pushing both the S&P 500 and Nasdaq to new record highs for the third consecutive week of gains

Wholesale inflation came in cooler than expected and regional manufacturing activity strengthened, though housing data remained weak and consumer sentiment continued to deteriorate

European and Japanese markets advanced as de-escalation sentiment broadened, China reported stronger than expected Q1 GDP growth of 5.0%

Economic Recap

U.S. economic data last week pointed to easing cost pressures alongside continued expansion in manufacturing activity. The Bureau of Labor Statistics reported that the PPI rose 0.5% month over month in March, below estimates for around a 1% rise and in line with February's revised increase, with the cooler reading driven by flat services inflation while a sharp increase in energy prices lifted goods inflation. Core PPI rose only 0.1%, down from 0.3% in February and below estimates for an increase of around 0.5%. Initial jobless claims for the week ended April 11 came in at 207,000, down from the prior week's revised reading of 218,000, while layoffs remained subdued overall. The New York Fed's Empire State Manufacturing Index rose to 11.0 in April from -0.2 in March, the highest since November, and the Philadelphia Fed's general activity index climbed to 26.7, its highest reading since January 2025, though employment turned negative and price measures rose to their highest levels since August.

Internationally, the IMF lowered its eurozone growth forecast to 1.1% for 2026, down from 1.3% in January, warning the Middle East conflict could trigger a major energy crisis without a durable resolution, and cut its UK forecast to 0.8% from 1.3%, the largest downward revision among G7 economies. The UK economy grew 0.5% month over month in February, stronger than the 0.1% expected, supported by administrative and support service activity. China's Q1 2026 GDP expanded 5.0% year over year, accelerating from 4.5% in the prior quarter and beating expectations, led by export strength and solid industrial output, though retail sales growth slowed to 1.7% year over year in March from 2.8% in the prior combined period, and property investment fell 11.2% in the first quarter. Germany's wholesale prices soared 4.1% year over year in March, driven primarily by energy and metals prices linked to the conflict.

Market Recap

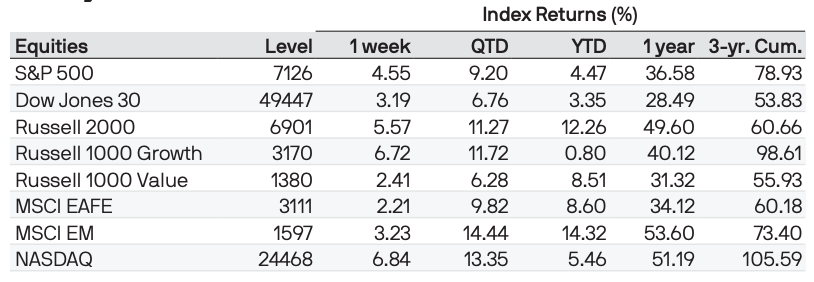

Source: JPMorgan Asset Management, “Weekly Market Recap” (April 20th, 2026). (Chart © JPMorgan Asset Management. Chart used under fair use for educational commentary by The Quinnipiac Global Economics Research Team.)

U.S. stocks posted strong gains for the third straight week, with several major indexes notching record highs amid signs of de-escalating conflict in the Middle East, upbeat early earnings results from major banks, and a series of generally positive economic data releases. The Nasdaq Composite led indexes higher with a gain of 6.84%, its longest winning streak since 1992, followed by the Russell 2000 at 5.57% and the S&P 500 at 3.58%. The S&P 500 is now up 4.47% year to date, recovering from its prior trough. Large-cap growth stocks outperformed for the third consecutive week, with the Russell 1000 Growth gaining 6.72% on the week and now up 0.80% year to date, while the Russell 1000 Value rose 2.41% and remains up 8.51% year to date. Energy was the only S&P 500 sector to post negative returns, while consumer discretionary, communication services, and information technology led gains. The catalyst for Friday's final leg higher was Iranian Foreign Minister Abbas Araghchi declaring the Strait of Hormuz completely open for commercial vessels following an Israel-Lebanon ceasefire agreement, which sent oil prices sharply lower to end the week at approximately USD 90 per barrel. U.S. 10-year Treasury yields dipped to 4.25%, though they remain more than 20 basis points above levels seen before the conflict began.

Internationally, the pan-European STOXX Europe 600 rose 1.91%, Germany's DAX added 3.77%, Italy's FTSE MIB rose 2.65%, and France's CAC 40 climbed 2.00%, while the MSCI EAFE gained 2.21% and MSCI EM advanced 3.23%. Japan's Nikkei 225 gained 2.73% and reached an all-time high, supported by AI enthusiasm and corporate governance themes regaining traction as geopolitical risk receded.

Market Themes

AI Capital Spending Estimates Surge as BlackRock Identifies a Supercharged Mega Force

BlackRock Investment Institute characterizes AI as a supercharged mega force, with conviction in the AI transformation growing on the back of three mutually reinforcing developments. First, consensus capital spending estimates for hyperscalers including Google, Meta, Microsoft, Amazon, and Oracle have risen over 25% since October 2025 across the 2026 to 2030 forecast window. Second, rapid revenue gains are materializing for AI model builders, with the Claude model maker Anthropic reporting a tripling of revenue to over USD 30 billion since the end of 2025. Third, U.S. tech valuations have fallen back in line with the broader S&P 500 even as tech earnings expectations have risen sharply, with the 12-month forward valuation of the U.S. IT sector relative to other sectors at its lowest level since mid-2020. BlackRock views this combination as underpinning its overweight to U.S. and emerging market equities and its preference for AI thematic opportunities in semiconductors, power, and data center infrastructure.

Hormuz Reopening and Hungary's Political Shift Illustrate Divergent Geopolitical Dynamics

While the dominant geopolitical narrative of recent weeks has centered on the Middle East conflict, last week saw two distinct geopolitical developments with meaningful market implications. The declaration by Iranian officials that the Strait of Hormuz was open during the Lebanon ceasefire provided the most direct relief to global markets. The durability of this opening remains contingent on the broader ceasefire framework holding, and BlackRock continues to monitor Hormuz shipping traffic through its proprietary tracker. Separately, Hungary's opposition leader Péter Magyar defeated Prime Minister Viktor Orbán in parliamentary elections, a development widely viewed as a potential turning point for Hungary's relationship with the European Union. According to T. Rowe Price Sovereign Analyst Peter Botoucharov, the result raises expectations of stronger growth and potential access to more than EUR 30 billion in frozen EU funds, with Hungarian equities, government bonds, and the forint all responding positively to the political transition.

Chart of the Week

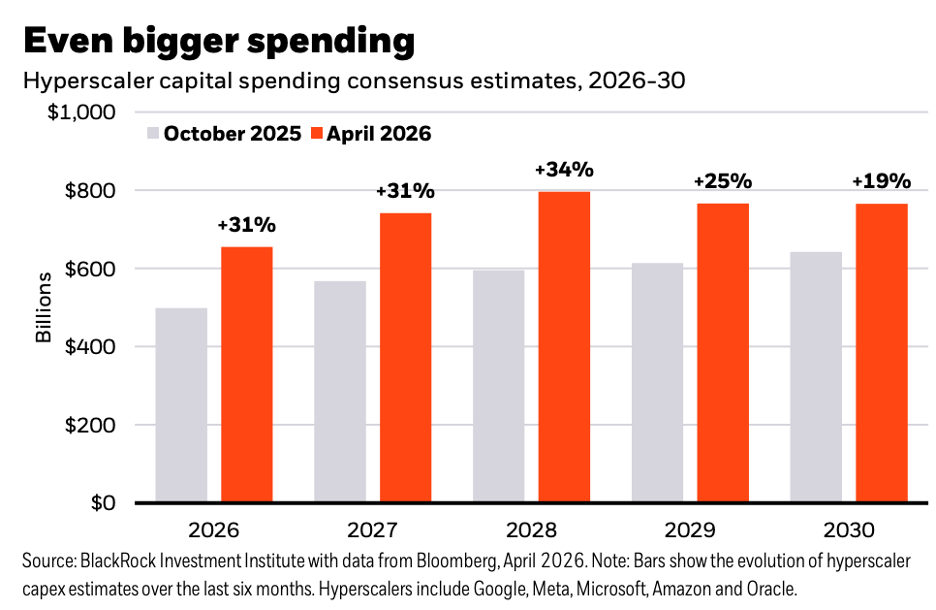

Source: BlackRock Investment Institute with data from Bloomberg, "Even Bigger Spending: Hyperscaler Capital Spending Consensus Estimates, 2026-30," April 2026. (Chart © BlackRock Investment Institute. Used under fair use for educational commentary by The Quinnipiac Global Economics Research Team.)

The chart compares hyperscaler capital spending consensus estimates for 2026 through 2030 at two points in time: October 2025 and April 2026. Across every year in the forecast window, April 2026 estimates are materially higher than those made just six months prior, with the largest upward revision occurring in 2028 at 34%, followed by 2026 and 2027 at 31% each, 2029 at 25%, and 2030 at 19%. In absolute terms, 2026 estimates now stand at approximately USD 660 billion, rising to approximately USD 750 billion in 2027 and approximately USD 800 billion in 2028 before moderating slightly. BlackRock notes this represents the fastest capital spending buildout in history, a trend it had already anticipated in its 2026 Global Outlook but which has since been reinforced by stronger than expected revenue growth at AI model builders and continued commitment to infrastructure investment by the world's largest technology companies. The chart provides a key underpinning for BlackRock's view that the AI mega force is accelerating rather than plateauing, supporting its overweight stance on U.S. equities and AI-linked thematic exposures.

Market Outlook

BlackRock Investment Institute will watch global flash PMIs this week for signs of any drag on growth from supply chain disruptions tied to the Middle East conflict. Japan's CPI and PPI data will also be closely monitored to assess whether the Bank of Japan can look through conflict-driven cost pressures and remain on track to achieve its 2% inflation target by the end of 2027. UK unemployment and inflation data will be the first such readings since the conflict began, and will highlight the Bank of England's inflation-growth trade-off. This week also brings the heaviest concentration of major technology earnings of the Q1 season, with Tesla, Microsoft, Meta, and Alphabet all reporting, providing the first direct evidence of whether AI capital spending commitments are translating into revenue growth and whether corporate guidance reflects confidence in continued buildout through the current geopolitical environment.

Calendar Events

Economic Data

Apr. 23 (Wed): Global Flash PMIs

Major Corporate Earnings

Apr.21 (Tue): GE Aerospace (Q1 2016)

Apr. 22 (Wed): Tesla Inc. (Q1 2026); AT&T Inc. (Q1 2026); The Boeing Company (Q1 2026)

Apr. 23 (Thu): Intel Corporation (Q1 2026)

Sources

J.P. Morgan Asset Management. "Weekly Market Recap." J.P. Morgan Asset Management. https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/market-

J.P. Morgan Asset Management. "Weekly Market Recap PDF." J.P. Morgan Asset Management. https://am.jpmorgan.com/content/dam/jpm-am-aem/americas/us/en/insights/market-insights/wmr/weekly_market_recap.pdf

J.P. Morgan Asset Management. "Economic Update." J.P. Morgan Asset Management. https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/market-updates/economic-update/

T. Rowe Price. "Global Markets Weekly Update." T. Rowe Price Insights. https://www.troweprice.com/personal-investing/resources/insights/global-markets-weekly-update.html

BlackRock Investment Institute. "Weekly Investment Commentary: A Supercharged AI Mega Force."

BlackRock, April 20, 2026. https://www.blackrock.com/us/individual/literature/market-commentary/weekly-investment-commentary-en-us-20260420-a-supercharged-ai-mega-force.pdf

BlackRock Investment Institute. "Weekly Commentary." BlackRock. https://www.blackrock.com/us/individual/insights/blackrock-investment-institute/weekly-commentary

BlackRock Investment Institute. "Weekly Commentary Archives." BlackRock. https://www.blackrock.com/corporate/insights/blackrock-investment-institute/archives

Apollo. "The Daily Spark." Apollo. https://www.apollo.com/wealth/the-daily-spark

MarketWatch. "Economic Calendar." MarketWatch. https://www.marketwatch.com/economy-politics/calendar

Yahoo Finance. "Earnings Calendar." Yahoo Finance. https://finance.yahoo.com/calendar/earnings/

Comments