CEE Exchange Rates Report for February 23rd – February 27th

- Mar 2

- 3 min read

By: Margaret Gachau, The Quinnipiac University Global Economics Research Team.

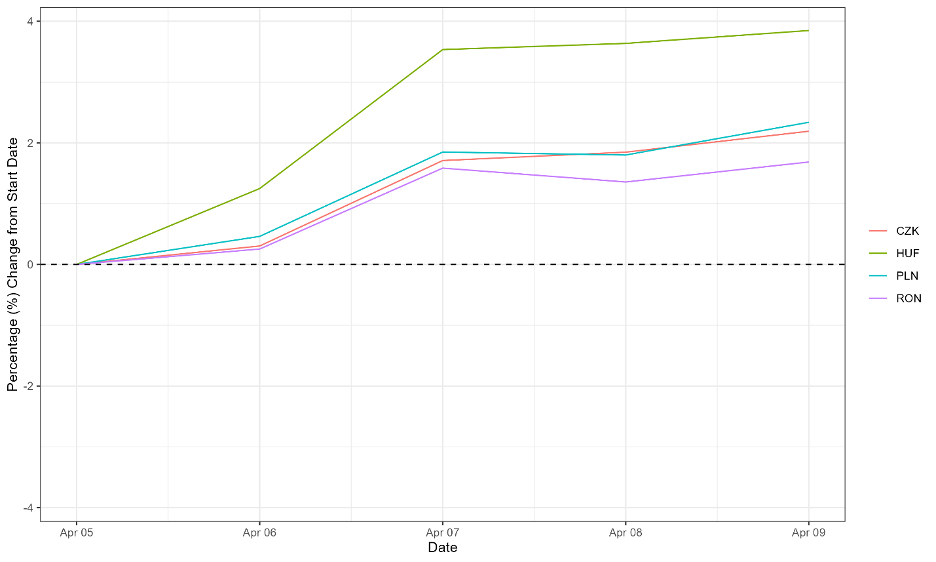

CEE Currencies Index

Source: Eurostat and own calculations. Exchange rates are inverted to be USD per local currency (i.e., an increase indicates a stronger domestic currency) and then indexed to be 100 at the start of the period.

During the last week of February 2026, Central and Eastern European (CEE) currencies exhibited a broadly depreciative trend against the U.S. dollar, with only modest stabilization toward the end of the week. All four currencies recorded net negative percentage changes by week’s close, although the magnitude and volatility differed across markets. The Hungarian forint (HUF) was the most volatile currency in the group. After a relatively mild early-week decline, it weakened sharply midweek, falling to approximately -1.9%, before partially recovering to close around -1.2%. In contrast, the Polish zloty (PLN), Romanian leu (RON), and Czech koruna (CZK) moved largely in tandem throughout the week, reflecting a shared regional dynamic. Their trajectories were closely aligned, with relatively contained fluctuations. By week’s end, both the koruna and zloty closed near -0.1%, while the leu ended slightly weaker at approximately -0.4%, following a brief midweek dip and modest late-week stabilization.

CEE Currencies Historical Trends

Source: Eurostat and own calculations. Exchange rates are inverted to be USD per local currency (i.e., an increase indicates a stronger domestic currency. The center line is a rolling three-month average. The upper and lower boundaries are the average plus and average minus one standard deviation, respectively, for the same three-month period

In the final week of February 2026, Central and Eastern European (CEE) currencies closed the month on a broadly weaker footing against the U.S. dollar. While the week initially reflected modest appreciation pressures, these gains reversed toward month-end, resulting in a generalized depreciative bias across the region. Relative to their three-month rolling averages, most currencies were trading below their upper bound levels by the end of the period. The notable exception was the Hungarian forint (HUF), which remained elevated and traded above its upper bound. At the country level, the Czech koruna (CZK) depreciated to approximately 0.0487 USD per koruna. The Hungarian forint strengthened earlier in the period, reaching around 0.00315 USD per forint, before edging slightly lower toward the week’s close. Similarly, the Polish zloty (PLN) advanced to roughly 0.280 USD per zloty, while the Romanian leu (RON) rose to approximately 0.232 USD per leu before both currencies reversed course and softened toward the end of the period.

Additional Reading

The Erste Group Research highlights diverging monetary policy trajectories across the CEE region. In Hungary, while the central bank is expected to hold rates at its upcoming meeting, easing is increasingly viewed as a matter of time given supportive inflation dynamics and exchange rate developments. In contrast, Romania’s central bank signaled a more cautious stance, postponing expected rate cuts until clearer evidence of sustained disinflation emerges—shifting projections from May to August and revising the year-end policy rate outlook upward.

Elsewhere, Poland is expected to begin easing in early March, Czechia is likely to maintain its 3.5% rate pending core inflation moderation, and Serbia is projected to gradually ease over the course of the year. Overall, FX markets remained relatively stable, though the Hungarian forint faced mild pressure amid uncertainty surrounding policy timing.

According to Reuters, the U.S. dollar is heading for its first monthly gain since October, supported by stronger-than-expected January producer price data and renewed geopolitical tensions between the U.S. and Iran. The Producer Price Index (PPI) rose 0.5% month-over-month, exceeding forecasts and reinforcing market unease about persistent inflation pressures. While some underlying components suggested moderation, the headline surprise strengthened the dollar earlier in the week.

Although the rally partially faded amid month-end positioning, the dollar index remains on track for a monthly increase, reflecting sustained inflation concerns and safe-haven demand. For emerging market currencies, including those in Central and Eastern Europe, this broader dollar resilience likely contributed to depreciation pressures observed toward month-end.

Comments