CEE Exchange Rates Report for March 2nd - 6th

- Mar 9

- 3 min read

By: Margaret Gachau, The Quinnipiac University Global Economics Research Team.

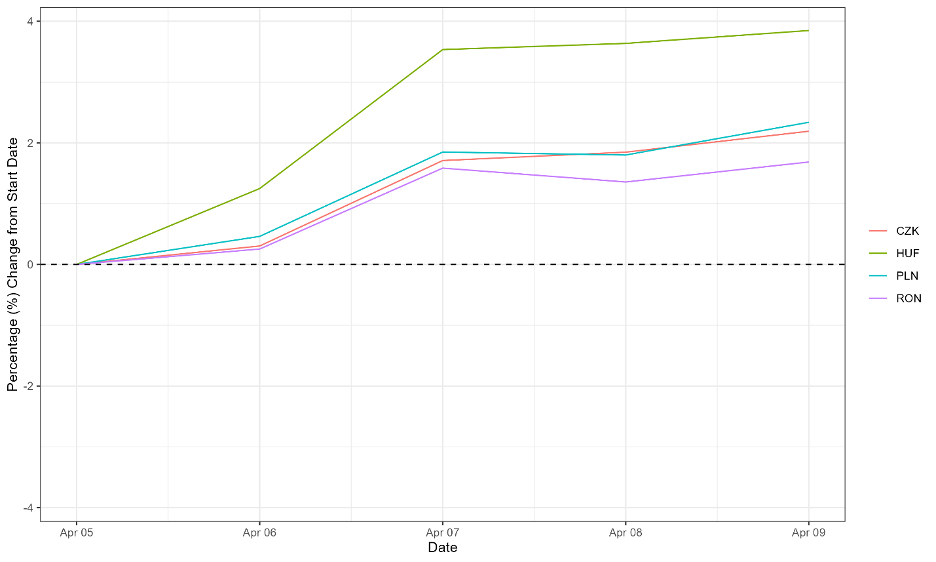

CEE Currencies Index

Source: Eurostat and own calculations. Exchange rates are inverted to be USD per local currency (i.e., an increase indicates a stronger domestic currency) and then indexed to be 100 at the start of the period.

During the week of March 2, 2025 – March 6, 2025, Central and Eastern European (CEE) currencies showed a broadly appreciating trend against the U.S. dollar, with gains building steadily over the course of the week despite a brief mid-week pullback. All four currencies recorded net positive percentage changes by the end of the period, although the magnitude of appreciation varied across markets. The Hungarian forint (green) was the most volatile currency strengthening rapidly early in the week, rising to nearly 4.8%, before briefly easing around mid-week to roughly 3.4%, and then rebounding strongly to close at approximately 6.7%. The Polish zloty (blue) followed a similar trajectory but with more moderate fluctuations. After climbing steadily to about 3.2%, it experienced a short-lived dip mid-week before recovering and ending the period near 3.6%. Meanwhile, the Czech koruna (orange) and Romanian leu (purple) moved largely in tandem throughout the week, reflecting shared regional dynamics. Both currencies posted gradual and relatively stable appreciation. By week’s end, the koruna reached roughly 2.9%, while the leu closed around 2.1%, maintaining the smallest but still consistent gains among the group.

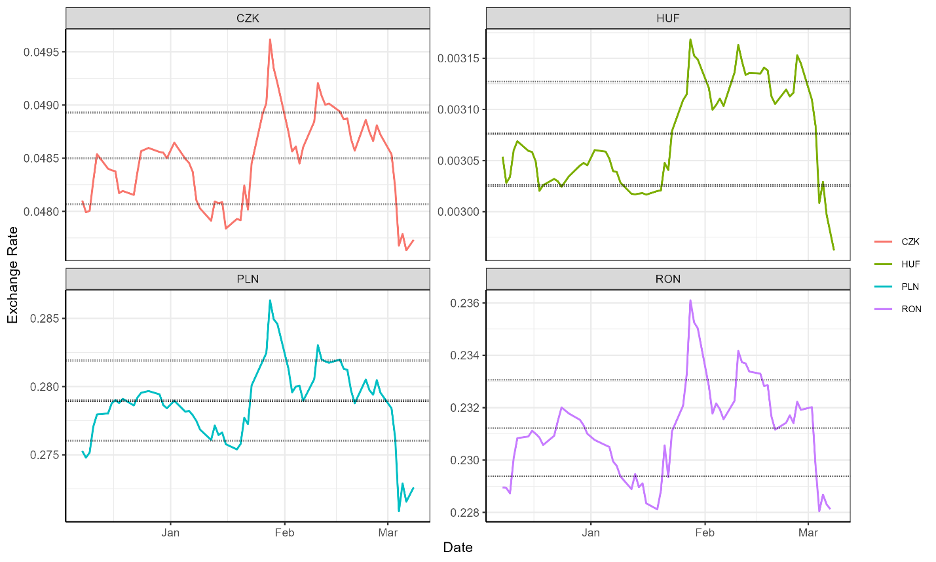

CEE Currencies Historical Trends

Source: Eurostat and own calculations. Exchange rates are inverted to be USD per local currency (i.e., an increase indicates a stronger domestic currency. The center line is a rolling three-month average. The upper and lower boundaries are the average plus and average minus one standard deviation, respectively, for the same three-month period

During the week of March 2, 2025 – March 6, 2025, Central and Eastern European (CEE) currencies moved lower against the U.S. dollar after earlier strength observed in early February. While several currencies had recently approached or exceeded their upper bound levels relative to their three-month rolling averages, the latest movements indicate a broad correction and renewed depreciation pressures across the region. By the end of the period, all currencies had fallen below their rolling averages and moved below their lower bound levels. At the country level, the Czech koruna (CZK) declined, falling to roughly 0.0477 USD per koruna, marking one of the sharpest late-period reversals. The Hungarian forint (HUF), which had earlier strengthened and briefly traded above its upper bound near also reversed course. It weakened significantly toward the end of the period, dropping to around 0.00297 USD per forint, moving below both its rolling average and lower bound range. Similarly, the Polish zloty (PLN) experienced a comparable pattern. The currency lost momentum and declined sharply, closing near 0.272 USD per zloty, well below its recent average. The Romanian leu (RON) followed a similar trajectory, it gradually weakened and fell to approximately 0.228 USD per leu by the end of the period. Overall, the synchronized downward movement across the currencies suggests renewed regional pressure and a stronger U.S. dollar environment influencing CEE exchange rates at the start of March.

Additional Reading

The article’s recent analysis suggests that rising geopolitical tensions in the Middle East have

increased energy prices, which may place additional pressure on Central and Eastern European (CEE) economies. Because many CEE countries are highly dependent on imported oil and gas, higher energy costs could push inflation higher and delay expected interest rate cuts by regional central banks. The shift toward higher inflation expectations and a stronger U.S. dollar has contributed to a more risk-averse market environment, putting downward pressure on regional currencies. Among CEE economies, Hungary and Romania are viewed as particularly exposed due to their higher sensitivity to energy price shocks and exchange-rate volatility

According to Reuters, Recent market developments suggest that escalating geopolitical tensions in the Middle East contributed to increased global financial market volatility in early March 2026. The widening conflict raised concerns about disruptions to oil supply through the Strait of Hormuz, pushing oil prices sharply higher and increasing inflation fears. As a result, investors shifted toward safe-haven assets, strengthening the U.S. dollar while global equity markets declined. The stronger dollar and heightened risk-off sentiment placed additional pressure on emerging-market currencies, including those in Central and Eastern Europe.

Comments